It’s Tuesday morning, and the MD at a £15M-turnover contractor has just opened the monthly report. Project A started with an 8% margin at tender – but six months in, nobody can say with confidence whether that margin still exists. The QS thinks so. The site manager isn’t sure. The spreadsheet says whatever was entered three weeks ago.

This guide covers how to forecast project profitability in construction – the core formula, what data feeds it, when and how often to forecast, the five structural reasons forecasts miss their targets, and how to improve accuracy over time. Written for QSs, commercial managers, and finance directors at UK contractors.

For the fundamentals of construction forecasting, start with What Is Construction Forecasting.

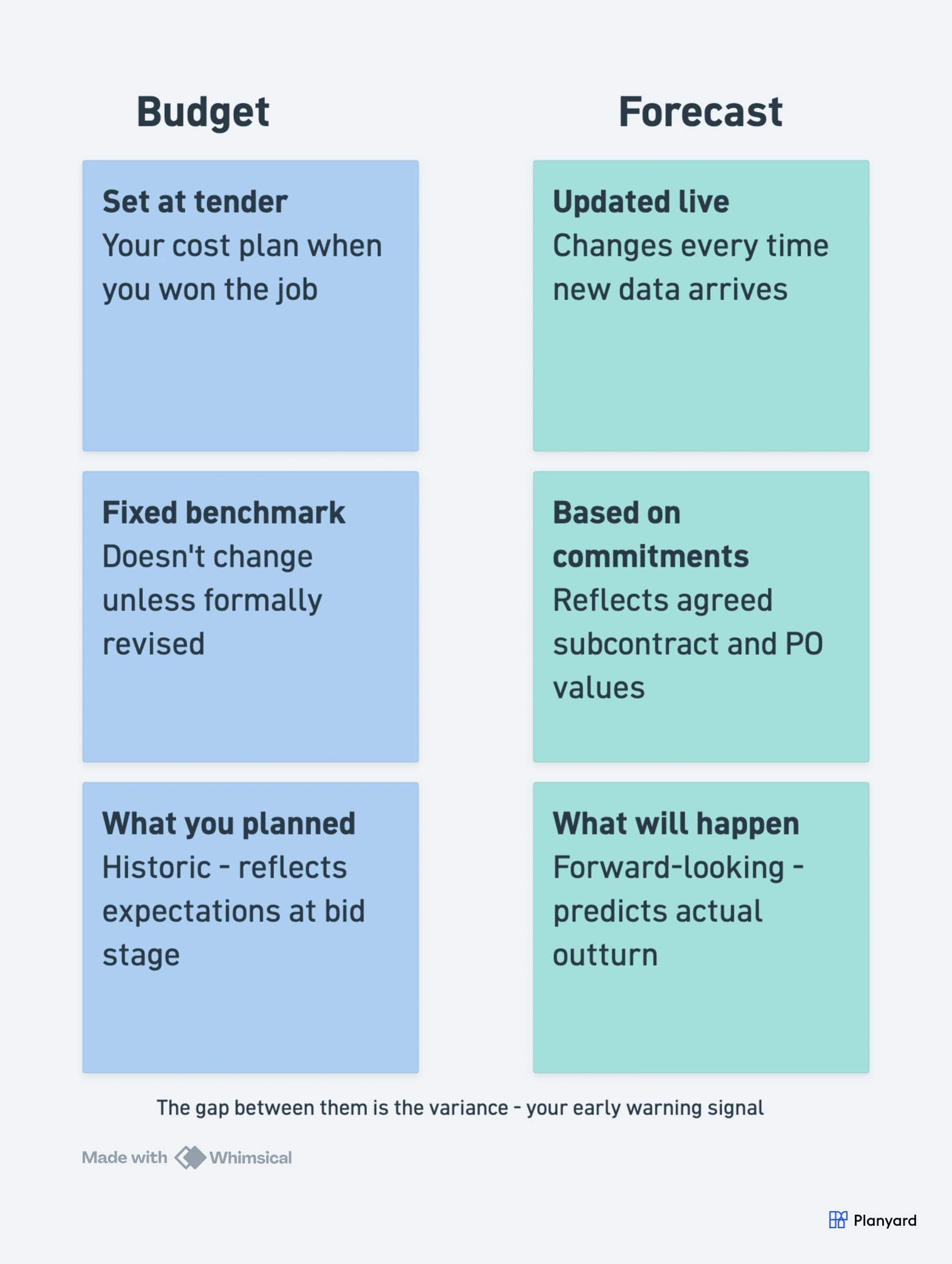

Why forecasting is not budgeting

Your budget is the cost plan you set at tender. It reflects what you expected to spend when you won the job. It’s fixed – a benchmark, not a prediction.

Your forecast is different. It’s a live prediction based on what you know today: which subcontracts have been let, at what values, what variations have been instructed, and what you still expect to spend on uncommitted work. The budget tells you what you planned. The forecast tells you what will actually happen.

The gap between them – the variance – is the signal. A forecast that exceeds the budget by 3% on a project with 6% planned margin means you’re heading for half the profit you expected. Catch it early enough, and you can act. Catch it at final account, and it’s too late.

The core formula

Profitability forecasting comes down to two numbers:

Forecast Final Cost = Committed Costs + Forecast Remaining Costs

Forecast Margin = (Contract Value – Forecast Final Cost) / Contract Value

A worked example:

- Contract value: £2,000,000

- Subcontracts let + POs raised (committed): £1,400,000

- Forecast remaining (uncommitted work): £480,000

- Forecast final cost: £1,880,000

- Forecast margin: (£2,000,000 – £1,880,000) / £2,000,000 = 6.0%

- Planned margin at tender: 8.0%

- Variance: -2.0% (margin erosion)

That 2% variance on a £2M job is £40,000 of profit at risk. Visible now – while there’s still time to investigate and act. Perhaps a package came in over budget. Perhaps a variation hasn’t been priced yet. The forecast surfaces the problem; the commercial team decides what to do about it.

For a deep dive on estimating the “forecast remaining” element, read our cost-to-complete forecasting guide.

"When you look at your margin without using Planyard, you might think you’re making 21%. But are you really if things have been missed and you can’t see them? Planyard lets you see a true margin all the time."

Read more

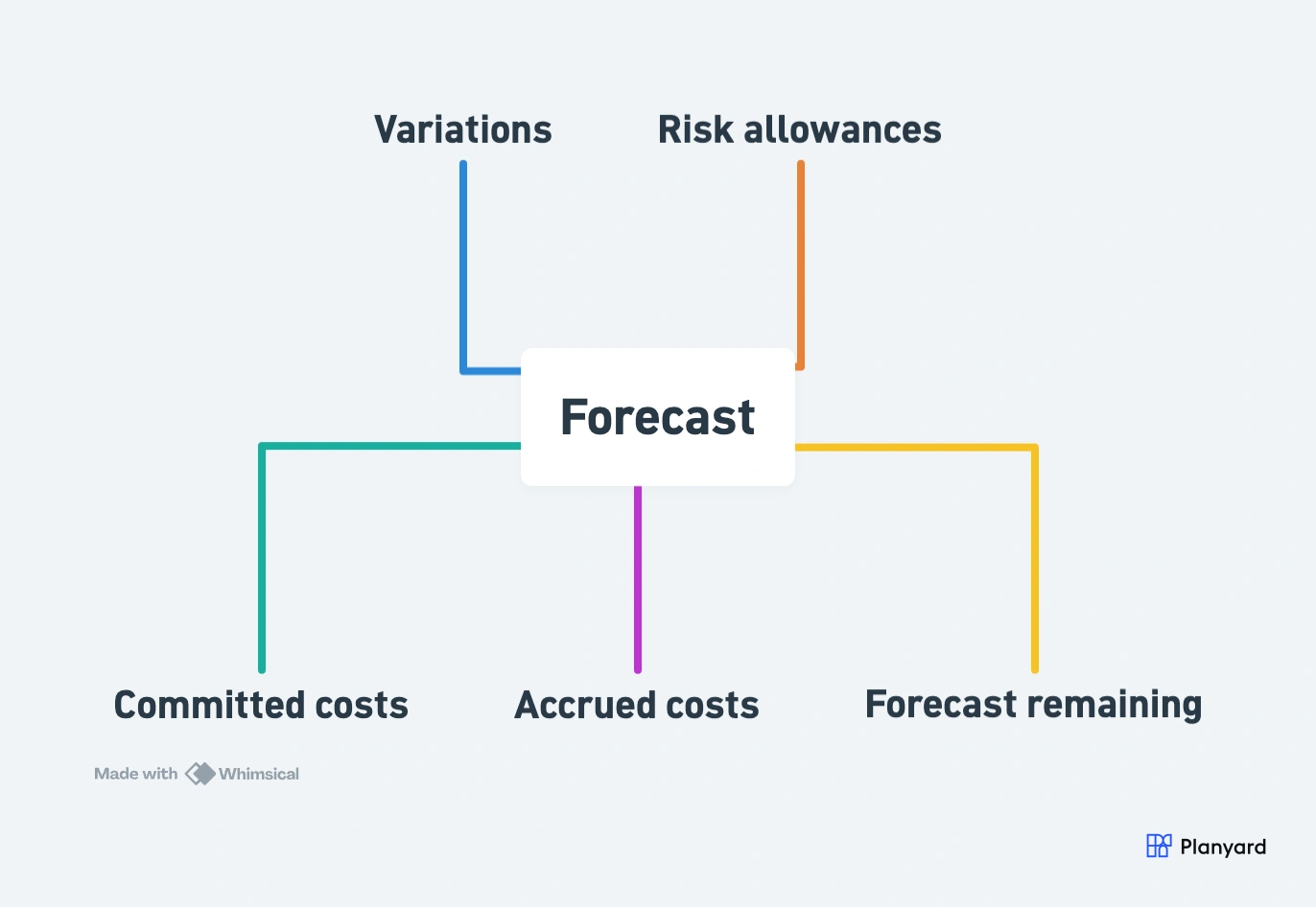

What goes into a good forecast

A forecast is only as good as its inputs. Here’s what you need to capture accurately:

Committed costs

Every subcontract awarded and purchase order raised. This is money you’re obligated to spend – the subcontractor will invoice you, whether it appears in your cost report yet or not. Commitments are the most reliable part of your forecast because they’re based on agreed prices, not estimates.

Read more about why commitments matter for forecasting.

Accrued costs

Work done but not yet invoiced. Your bricklayer finished last week’s work but their application won’t arrive for another fortnight. You need to account for this in your cost position – otherwise you’re understating what you owe.

Forecast remaining

The uncommitted work still to procure. This is the uncertain part – you’re estimating what you’ll spend on packages not yet let, materials not yet ordered, and labour not yet allocated. As the project progresses and more work gets committed, this figure shrinks and your forecast becomes more certain.

Variations

Both approved (agreed value, confirmed scope) and anticipated (instructed but not yet priced). Variations affect both sides: the contract value (income) and the forecast cost. Log them early, even if the value is provisional.

Risk allowances

Contingency should reflect project stage and known risks. Early in the project, carry more contingency. As packages are let and prices confirmed, contingency should reduce. If it doesn’t, you’re either being too cautious or you haven’t updated the forecast.

When and how often to forecast

The minimum frequency is monthly – aligned with your CVR (cost value reconciliation) cycle. But monthly is the floor, not the ceiling.

Update the forecast immediately after:

- Every major subcontract award (especially if the value differs from budget)

- Change events – variation instructions, design changes, programme delays

- Material price confirmations that differ from allowances

- Any event that materially changes your cost expectation

As the project progresses, forecast frequency should increase. You have more data, more committed packages, and less remaining uncertainty. The forecast gets more reliable – but only if you keep it current.

"As project managers, we need to know that the budget we’ve been given is being tracked accurately so we aren't overspending. Our goal is to ensure that when the next month rolls around, there are absolutely no surprises. Having that continuous visibility means we can stay on top of the numbers and keep the project on track."

Read more

Five reasons forecasts miss profitability targets

Even teams that forecast regularly can miss their targets. Here are the structural reasons – not mistakes of effort, but mistakes of method:

1. Ignoring uncommitted costs

Only counting what’s been invoiced means you’re looking at the past, not the future. Committed but uninvoiced costs are real obligations – they belong in the forecast from the day of award.

2. Optimism bias on remaining work

“We’ll make it back on the next package.” This is the most dangerous sentence in construction commercial management. If your subcontractors are coming in over budget on the packages you’ve already let, why would the remaining ones be different?

3. Not capturing variations early enough

The instruction has been issued. The work is being done. But the variation hasn’t been priced or logged in the forecast. Weeks pass – costs incur – and when the variation finally lands, it’s a “surprise”. It shouldn’t be.

4. Failing to update after scope changes

Design changes, programme acceleration, late architect information – all change your cost base. If the forecast doesn’t move when scope moves, it’s no longer a forecast. It’s last month’s guess.

5. Using outdated subcontractor quotes

Your forecast shows £80K for the M&E package because that’s what the tender estimate said. But that estimate is six months old, the market has moved, and the actual quotes coming in are £95K. Until you update the forecast to reflect current pricing, you’re underestimating final cost.

For a deeper exploration of these failure modes, read why construction forecasts are always wrong.

Stop discovering margin problems at final account

Track committed costs and forecast margin in real time. 14-day free trial, no card required.

How to improve forecast accuracy over time

Forecasting is a skill. It improves with feedback loops and accountability:

- Post-mortem comparison: at project completion, compare your forecast at each stage to the actual outturn. Where did it drift? Why?

- Track accuracy as a KPI: measure forecast accuracy across projects. Which project types are harder to forecast? Which QSs are more accurate?

- Connect commitments to forecasts automatically: remove the manual step of entering committed costs into the forecast. When the PO is raised, the forecast should update.

- Involve site teams: the people doing the work know what’s coming. Monthly reviews should include site input on cost-to-complete estimates for their trades.

"Klaus can confirm that after the implementation of Planyard, there have been no projects where the financial results at the end of the project contained surprises."

Read more

Tools and process

Spreadsheets work for forecasting – until they don’t. The inflection point is usually when you’re running 5+ live projects and your QS is spending days compiling data rather than analysing it.

The problems with spreadsheet-based forecasting:

- No live connection to commitments – POs and subcontracts must be manually entered

- Version control breaks down with multiple users

- No audit trail – who changed what, when?

- One person’s holiday = one month of stale data

Construction forecasting software solves this by connecting budget, commitments, invoices, and forecast in a single system. When you raise a PO, the committed cost feeds the forecast automatically. When an invoice arrives and matches an order, the actual vs committed position updates in real time.

Teams typically cut forecast preparation from days to minutes and get started on a live project in under an hour. Variance alerts flag problems before they compound.

For contractors using Xero for their accounting, Planyard integrates directly – giving you project-level forecasting on top of your existing accounting setup without replacing it.

"If I were still relying solely on Excel to track and present the financial positions of our projects, I would be losing significant time every single month. By implementing the streamlined processes that Planyard supports, I’m saving at least three to four days of work every month that would have otherwise been spent on manual data entry and reconciliation."

Read more

Cash flow vs profitability: a critical distinction

A project can be profitable on paper but cash-negative for months. Profitability tells you whether the project will make money overall. Cash flow tells you whether you’ll have money in the bank at each point along the way.

They require different forecasts and different actions. This guide focuses on profitability forecasting. For cash flow, read our dedicated guide to forecasting cash flow in construction.

Summary: the forecasting discipline

Forecasting project profitability isn’t an academic exercise – it’s the core commercial discipline that separates contractors who control their margins from those who discover them at completion. The formula is simple. The discipline is in the inputs: tracking commitments from day one, updating when things change, and reviewing with rigour rather than optimism.

Start with committed costs. Update on every change event. Review monthly with site input. Compare forecast to budget and investigate variances. That’s the process. Everything else is tooling.

Forecast profitability from committed costs automatically

Live margin tracking for contractors. See forecast updates the moment you raise a PO.