Accurate financial records are essential for construction companies to track project costs, stay within budget, and provide clarity for stakeholders. Construction projects require a specialized approach known as Construction in Progress (CIP) accounting. This method allows companies to manage expenses for ongoing projects, keeping finances organized until completion. In this guide we’ll explore CIP accounting in construction, its representation on the balance sheet, and how Planyard can streamline the process.

What Is Construction in Progress?

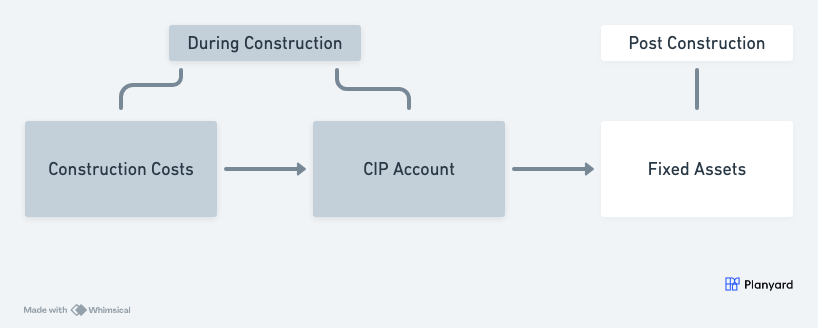

Construction in Progress (CIP) is an accounting term used to track costs associated with building long-term assets like commercial buildings, office complexes, or infrastructure projects. These expenses are recorded in a CIP account, holding a natural debit balance within the Property, Plant, and Equipment (PP&E) section on the balance sheet.

CIP is classified as an asset rather than an expense, representing the company’s investment in ongoing projects. This classification separates CIP from operating expenses, highlighting financial commitments toward incomplete projects. Since construction projects are often multi-phase and lengthy, CIP accounting monitors these costs as assets, simplifying capital investment tracking. When a project is complete, the cumulative CIP balance transfers to a fixed asset account, and depreciation begins.

Difference Between CIP and WIP Accounting

While CIP and Work in Progress (WIP) accounting may sound similar, they serve different purposes:

- Construction in Progress (CIP): Used specifically for construction projects to track costs for long-term assets like buildings. These costs are treated as assets under PP&E on the balance sheet.

- Work in Progress (WIP): Common in manufacturing to track costs of goods still in production. WIP costs are classified as inventory until items are completed.

So, CIP focuses on construction assets, whereas WIP deals with inventory in production.

The Importance of CIP Accounting

Better Financial Control

CIP accounting keeps construction expenses organized and distinct from daily operating costs. This organization allows project managers to assess financial health at each stage and make informed decisions.

"We are now able to forecast and see exactly how we performed against our original estimates. It keeps all of our documents and financial data in one central place, which allows anyone on the team to jump in and instantly see the status of any line item, when it was paid, and the actual documentation behind those payments."

Read more

Transparency for Investors and Auditors

It ensures clarity for stakeholders and auditors by providing an accurate view of active commitments in ongoing projects. By separating construction investments, CIP maintains clear financial records that comply with accounting standards like GAAP.

"We once sent out a cost plan to a client with a significant sum missing. That creates immediate tension and mistrust, which can lead to serious issues in the relationship."

Read more

Effective Cost Control and Budgeting

Tracking costs in CIP accounts helps monitor project expenses closely, identify potential budget issues, and make necessary adjustments early. This proactive approach supports better budgeting and financial planning for future projects.

"It’s a fantastic visualizer; you can jump onto Planyard at any point and instantly see exactly how the job is performing straight away."

Read more

How to Record and Capitalize CIP Expenses

Construction in Progress is capitalized as part of the company’s assets. Expenses directly associated with the project—such as materials, labor, and permits—are recorded in the CIP account during construction. These costs remain in CIP until project completion, then transfer to a fixed asset account, and depreciation begins. This approach treats CIP expenses as assets, reflecting ongoing investment in long-term projects.

Handling CIP Accounting:

Step 1: Identify CIP Expenses

Include only costs directly tied to a specific project:

- Building materials (e.g., concrete, steel, lumber)

- Labor costs

- Subcontractor fees

- Permits and licenses

- Installation and equipment usage fees

- Interest on project-related loans

Recording these expenses as assets creates a complete record of capital investment throughout the project.

Step 2: Document and Record Each Expense

Detailed documentation—receipts, invoices, records—is crucial for accuracy and audit readiness. This ensures the project’s financial history is fully captured, simplifying auditing and compliance.

Step 3: Log Expenses in the CIP Account

Enter each expense as a debit in the CIP account and a credit in accounts payable. For example, receiving steel beams worth $35,000:

- Construction in Progress (Debit): +$35,000

- Accounts Payable (Credit): -$35,000

This method keeps the CIP account balanced and accurately reflects total project costs.

Step 4: Transfer CIP to Fixed Assets Upon Completion

When the project is complete, transfer the CIP balance to a fixed asset account like “Buildings.” This signifies the asset’s transition to operational use, and depreciation begins.

Practical CIP Checklist

- Identify Project Expenses:

- Track expenses specific to each project:

- Materials

- Labor wages

- Subcontractor fees

- Permits and licenses

- Equipment usage fees

- Loan interest

- Track expenses specific to each project:

- Document Each Expense:

- Gather receipts, invoices, and records.

- Store documents for easy audit access.

- Log Expenses in the CIP Account:

- Record each expense as a debit in CIP.

- Balance with a credit in accounts payable.

- Transfer CIP to Fixed Assets at Completion:

- Move the CIP balance to a fixed asset account to start depreciation.

- Ensure Compliance with Standards:

- Periodically review entries to meet GAAP or other standards.

How CIP Is Represented on the Balance Sheet

CIP appears under the Property, Plant, and Equipment (PP&E) section, reflecting the value of ongoing construction projects. The CIP balance shows capital investment in active projects, offering stakeholders insight into ongoing commitments.

Is Construction in Progress a Fixed Asset?

Yes, CIP is considered a fixed asset on the balance sheet. Despite not being completed or operational, it’s recorded within the PP&E section, encompassing long-term assets used to generate revenue over multiple periods. CIP represents capital investment in assets under construction, expected to provide future economic benefits. During construction, CIP is not depreciated because it’s not yet available for use. All direct project costs are accumulated in the CIP account and transferred to the appropriate fixed asset account upon completion, where depreciation begins.

Importance of CIP Classification

- Reflects Ongoing Investment: Acknowledges investment in assets contributing to future revenue.

- Financial Statement Accuracy: Ensures the balance sheet accurately reflects all assets.

- Compliance with Accounting Standards: GAAP requires capitalizing expenditures for assets under construction.

Transitioning CIP to a Fixed Asset Account

Upon project completion, the CIP balance is reclassified to a fixed asset account, formally designating the asset as operational. For example, completing an office complex transfers accumulated CIP costs to a “Buildings” account under PP&E. This enables depreciation to begin, distributing the asset’s cost over its useful life.

This transition is essential for:

- Compliance with Standards: Adhering to GAAP and providing a clear financial structure.

- Accurate Financial Reporting: Reflecting completed projects as revenue-generating investments.

- Audit Readiness: Maintaining documentation for transparency.

Example of CIP Accounting in Action

Let’s examine a scenario: a construction company records costs incurred during the development of an office complex, detailed below:

| Date | Description | Amount | Journal Entry |

| Jan 15, 2024 | Purchase of concrete and steel for foundational work | $25,000 | Debit: Construction in Progress (+$25,000)Credit: Accounts Payable (–$25,000) |

| Feb 3, 2024 | Payment to contractors for initial construction work | $50,000 | Debit: Construction in Progress (+$50,000)Credit: Accounts Payable (–$50,000) |

| Feb 25, 2024 | Architectural services and structural engineering costs | $12,000 | Debit: Construction in Progress (+$12,000)Credit: Accounts Payable (–$12,000) |

| Mar 10, 2024 | HVAC and electrical wiring installations | $40,000 | Debit: Construction in Progress (+$40,000)Credit: Accounts Payable (–$40,000) |

| Apr 15, 2024 | Painting, flooring, and final inspections | $20,000 | Debit: Construction in Progress (+$20,000)Credit: Accounts Payable (–$20,000) |

| May 1, 2024 | Transfer of completed project to fixed assets for depreciation | $147,000 | Debit: Buildings (Fixed Asset) (+$147,000)Credit: Construction in Progress (–$147,000) |

Cumulative CIP total calculation:

To date, the total amount in the CIP account is the sum of all debited amounts:

- $25,000 (materials)

- $50,000 (contractors)

- $12,000 (architecture)

- $40,000 (HVAC and electrical)

- $20,000 (finishes)

Total CIP Balance: $25,000+$50,000+$12,000+$40,000+$20,000=$147,000

As costs are recorded, the cumulative CIP balance grows. Upon project completion, the company transfers the CIP balance to the “Buildings” fixed asset account, and depreciation begins.

CIP Accounting Standards and Compliance

Following Generally Accepted Accounting Principles (GAAP) is essential for the correct and transparent handling of CIP. GAAP provides standards that regulate financial data recording and reporting, ensuring consistency and fairness. GAAP standards are crucial in CIP accounting for:

- Accurate Asset Classification: Construction costs related to CIP must be recorded under PP&E.

- Preventing Premature Revenue Recognition: Companies can’t recognize revenue or depreciate assets before they’re operational.

- Consistency Across Reporting Periods: Uniform financial data reporting facilitates better investor communication.

- Improved Audit Readiness: GAAP compliance prepares companies for audits with clear CIP tracking standards.

- Regulatory Compliance: Aligning CIP accounting with GAAP reduces legal risks.

Mitigating Common Challenges in CIP Accounting

CIP accounting in construction presents unique challenges, but effective strategies can ensure accurate financial reporting.

Long Project Timelines

Projects spanning multiple accounting periods complicate expense tracking and reporting.

Mitigation Strategies:

- Implement Robust Accounting Systems: Use software that handles multi-period projects.

- Regular Financial Reviews: Reconcile accounts periodically to address discrepancies.

- Effective Communication: Maintain alignment between project managers and accounting teams.

- Milestone Billing: Break projects into milestones to manage cash flow and tracking.

Budget Overruns

Unplanned costs from price changes or delays affect CIP accuracy and profitability.

Mitigation Strategies:

- Contingency Planning: Include contingency funds for unexpected expenses.

- Real-Time Cost Monitoring: Use tools for immediate expense updates to identify overruns.

- Vendor Agreements: Negotiate fixed-price contracts to lock in costs.

- Risk Management: Conduct risk assessments to anticipate and mitigate delays or cost increases.

"Planyard takes your project budget and puts it very clearly on screen, allowing you to account for all your costs, invoices, and receipts as you process them before they even reach the accounting department. This gives you a live, real-time picture of exactly where your project budget stands at any given point."

Read more

Compliance and Audits

Strict adherence to GAAP requires meticulous documentation and accounting principles.

Mitigation Strategies:

- Maintain Detailed Records: Keep comprehensive documentation of all transactions.

- Staff Training: Ensure accounting personnel are knowledgeable about GAAP and CIP practices.

- Internal Audits: Regularly audit internally to correct discrepancies before external audits.

- Automate Compliance Processes: Implement software that enforces compliance rules and provides audit trails.

Financial Implications of CIP Accounting

CIP assets represent significant future investments enhancing operational capacity and financial value. Upon completion, CIP assets transition to fixed assets, impacting:

- Balance Sheet and Asset Valuation: Accurate capitalization reflects ongoing projects and investments.

- Depreciation and Expense Recognition: Fixed assets enter depreciation schedules, spreading expense recognition.

- Financial Ratios and Creditworthiness: Capitalized CIP assets can improve ratios like asset turnover and return on assets (ROA).

- Cash Flow and Budgeting: Operational assets generate cash flows, contributing to revenue streams.

- Investor Confidence: Clear CIP accounting demonstrates growth prospects and capital investments.

Whether managing commercial, residential, or infrastructure projects, Construction in Progress accounting — paired with the right tools — ensures every project investment is accurately captured from start to finish.

"When you look at your margin without using Planyard, you might think you’re making 21%. But are you really if things have been missed and you can’t see them? Planyard lets you see a true margin all the time."

Read more

Planyard streamlines CIP accounting by making it easier to stay organized, reduce manual errors, and keep each project’s financial status clear. It simplifies tracking so you can confidently manage budgets and ensure accurate, reliable financial records — all while focusing on successful project delivery.