CIP accounting is a pivotal process for businesses handling construction or asset projects. This guide will break down its meaning, importance, and practical applications while addressing common challenges and solutions. Whether you’re a contractor, financial manager, or accountant, understanding CIP accounting ensures accurate financial reporting and effective project cost control.

What is CIP in Accounting?

CIP accounting refers to the practice of tracking and recording costs associated with incomplete construction projects. It is essential to ensure that costs are allocated correctly and transparently during the construction phase of an asset.

CIP stands for “Construction in Progress” in accounting and is used to track costs like materials, labor, and overhead expenses before the asset is complete. These costs are recorded in a CIP account, which is categorized as a non-depreciable fixed asset on the balance sheet. Once the project is finished, the total costs are transferred to the appropriate asset account, and depreciation begins.

By maintaining a dedicated CIP account, businesses can avoid mixing incomplete project costs with operational expenses, ensuring accurate financial reporting. This separation also allows project managers and stakeholders to monitor progress and spending in real-time, making adjustments as necessary to avoid cost overruns.

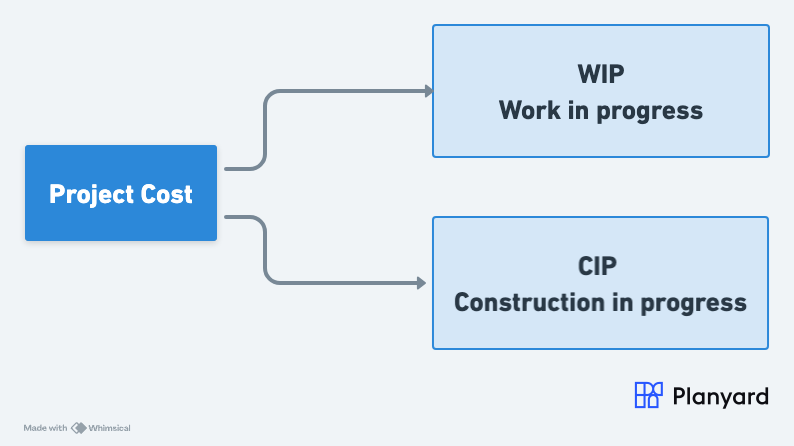

CIP vs. WIP Accounting: Key Differences

While both CIP and WIP (Work in Progress) accounting deal with ongoing projects, they serve different purposes. CIP is used for fixed-asset construction projects, such as buildings or infrastructure, while WIP tracks costs for operational projects or production processes, such as manufacturing.

Key differences include the type of project tracked and how costs are reported. CIP accounts reflect capital investments and appear as fixed assets, while WIP costs are reported under inventory on the balance sheet. Both are essential for accurate financial reporting, but understanding their distinct roles ensures clarity in financial statements.

Additionally, WIP accounts often deal with short-term projects with a direct impact on inventory turnover, while CIP is more suited for long-term investments that can span years. This distinction makes CIP a crucial accounting tool for industries like construction, where large-scale projects require meticulous financial oversight.

CIP on the Balance Sheet

CIP is categorized as a fixed asset on the balance sheet. However, unlike other fixed assets, CIP does not undergo depreciation until the construction is complete, and the asset is put into use. This makes CIP unique in financial reporting.

For example, if a company is constructing a new office building, all related costs—such as architectural fees, materials, and labor—are recorded under the CIP account. Once the building is finished, the total cost is transferred to the “Buildings” account, where it begins to depreciate.

Properly managing CIP on the balance sheet ensures accurate reporting of an organization’s financial position and prevents misstatements that could affect decision-making.

How to Record CIP in Accounting

Recording CIP involves several critical steps to ensure accurate tracking and reporting:

| Step | Action | Example |

| 1. Identify Costs | Track all expenses related to construction. | Material costs, labor, and overhead. |

| 2. Update Regularly | Add ongoing costs to the CIP account. | Weekly updates for transparency. |

| 3. Transfer Costs | Move completed project costs to fixed assets. | Transfer $500,000 to “Building Assets.” |

| 3. Transfer Costs | Begin depreciating the completed asset. | Depreciate building costs over 30 years. |

For example, if a company spends $500,000 on constructing a warehouse, those costs are tracked in the CIP account until the warehouse is operational. At that point, the costs are transferred to the “Warehouse” fixed asset account.

Challenges in CIP Accounting

CIP accounting can be complex due to the sheer volume of costs involved and the need for accurate allocation. Common challenges include:

- Manual errors: Using spreadsheets to track costs can result in inaccuracies.

- Delayed updates: Incomplete or delayed entries can distort financial reporting.

- Cost misallocation: Incorrectly categorizing costs can lead to compliance issues and financial misstatements.

These challenges can result in financial inaccuracies that disrupt project timelines or budgets. Businesses should focus on implementing systems that automate these processes to ensure efficiency and reduce the risk of errors.

Why It Matters

For construction companies, CIP accounting is more than just a financial practice—it’s a strategic tool. Accurate tracking of project costs helps:

- Ensure project profitability: Avoid cost overruns and monitor budgets in real-time.

- Streamline financial reporting: Maintain transparency and accuracy in balance sheets.

- Improve decision-making: Access up-to-date financial data to guide strategic planning.

Moreover, businesses that excel in CIP accounting can improve client trust by demonstrating financial discipline and a clear understanding of project finances, giving them a competitive edge in the market.

Best Practices for CIP Accounting

To maximize the effectiveness of CIP accounting and minimize risks, implement these best practices:

- Centralize documentation: Store all project cost records in a single, easily accessible system to avoid losing critical data.

- Adopt Construction Accounting Software: Leverage construction-specific accounting software to automate cost tracking, budget updates, and invoice management, ensuring accuracy and real-time updates tailored to project needs.

- Conduct regular audits: Periodically review CIP accounts to identify discrepancies early and ensure compliance with accounting standards.

- Integrate with financial systems: Link CIP tracking with accounting tools like QuickBooks or Xero to streamline reporting and eliminate manual errors.

- Train your team: Equip project managers and financial staff with the knowledge to handle CIP accounts effectively.

These practices not only enhance accuracy but also improve overall financial management for ongoing and future projects.

Planyard: A Smarter CIP Accounting Solution

Managing CIP accounting manually can be time-consuming and prone to errors. Planyard offers an intuitive solution designed to simplify the process for construction professionals.

With Planyard, you can:

- Automatically track project costs in real-time.

- Seamlessly integrate with popular accounting tools like QuickBooks and Xero.

- Generate instant financial reports with accurate CIP data.

- Reduce manual errors by automating workflows such as invoice matching and purchase order tracking.

For example, Planyard automatically updates budgets as costs are recorded, ensuring real-time accuracy without the need for redundant data entry. These features help businesses stay on top of their financials and maintain profitability throughout the project lifecycle.

Conclusion

CIP accounting is a critical aspect of financial management for construction and asset-intensive businesses. By understanding its principles, adopting best practices, and leveraging tools like Planyard, you can ensure accurate cost tracking, enhance transparency, and make informed financial decisions.

Take the next step in streamlining your project cost management—start your free trial with Planyard today or schedule a demo to experience the difference in real-time financial control.