In the construction industry—especially under the Design and Build procurement route—the Contract Sum Analysis (CSA) is an essential but often misunderstood tool. Whether you’re pricing a job, submitting a tender, or managing interim payments, a well-structured CSA can mean the difference between smooth progress and payment disputes.

The CSA isn’t just about ticking boxes—it’s about protecting your margins, maintaining transparency, and keeping the project financially on track.

This guide covers the fundamentals of the CSA, key differences between pricing methods, associated risks, and best practices for both contractors and developers.

What Is a Contract Sum Analysis?

A Contract Sum Analysis is a pricing breakdown used predominantly in Design and Build projects. It itemises the contractor’s lump sum price across work sections, allowing the Employer’s Agent and Quantity Surveyor to:

- Compare tender submissions more effectively

- Assess interim valuations during construction

- Establish a basis for measuring variations

Since Design and Build contracts rarely include a full Bill of Quantities (BoQ), the CSA becomes the key pricing document and is formally referenced in JCT Design and Build contracts under Article 4.

What Is Included in the Contract Sum?

The Contract Sum includes all known and quantifiable costs for delivering the employer’s requirements. This typically covers:

- Direct construction costs (labour, plant, materials)

- Preliminaries (management, welfare, temporary works)

- Overheads and profit

- Provisional sums (where defined)

- Contingency (if applicable)

- Design development allowances (if agreed)

Exclusions include:

- Variations and changes post-contract

- Compensation events

- Scope not clearly identified in the Employer’s Requirements

Lump Sum vs Time & Materials (T&M): Key Differences

These are two different methods of pricing and payment:

Lump Sum:

- A fixed total price is agreed upon for completing the project. This is the most common in Design and Build and is where the CSA is typically used.

- The contractor takes on more risk—if costs overrun, they absorb the difference (unless it’s due to a variation).

Time & Materials (T&M):

- Payment is made based on actual time spent and materials used, often with a markup for overhead and profit.

- This method offers more flexibility but less cost certainty for the client.

In essence, Lump Sum = fixed price, higher contractor risk, whereas T&M = open-ended cost, higher client exposure.

What Is the Effective Contract Sum?

The Effective Contract Sum refers to the total contract price after adjustments, such as:

- Agreed variations

- Omitted or added scope

- Re-assessed provisional sums

- Extensions of time with cost implications

- Adjustments due to design development

It reflects the real financial commitment of the employer as the project evolves. While the original Contract Sum is fixed at contract signing, the Effective Contract Sum tracks its actual movement over the life of the project.

CSA vs BoQ – What’s the Difference?

A Bill of Quantities (BoQ) is typically prepared by the employer or their consultants as part of the tender documents. It outlines detailed quantities, specifications, and pricing structures for the project. The main purpose of the BoQ is to provide a consistent basis for contractors to price the works during tendering.

On the other hand, a Contract Sum Analysis (CSA) is usually produced by the contractor, based on the design information available at the time of tender. It reflects how the contractor has built up their tender price, including assumptions and breakdowns that support the contract sum.

In Design and Build contracts, where different contractors may interpret the BoQ differently or even use third-party estimators, the CSA becomes essential. It ensures there is transparency and alignment in how the price is structured—making it easier to assess and compare tenders.

Key difference: The BoQ helps in pricing during tender, but only the CSA forms part of the contract(unless the BoQ is explicitly included).

CSA Layout – High-Level vs Detailed

| Section | High-Level CSA Entry | Detailed CSA Entries |

| Substructure | Substructure – £150,000 | Excavation – £25,000 Piling – £75,000 Ground slab – £50,000 |

| Superstructure | Superstructure – £400,000 | Steel frame – £150,000 Upper floors – £120,000 Roof – £130,000 |

| Internal Finishes | Internal Finishes – £120,000 | Wall finishes – £45,000 Floor finishes – £50,000 Ceilings – £25,000 |

| M&E Services | M&E – £300,000 | Electrical – £100,000 HVAC – £120,000 Plumbing – £80,000 |

| External Works | External Works – £100,000 | Landscaping – £40,000 Drainage – £30,000 Paving – £30,000 |

| Preliminaries | Prelims – £90,000 | Site setup – £20,000 Management – £55,000 Welfare – £15,000 |

| OHP & Contingency | OHP – £90,000 | Overheads – £50,000 Profit – £20,000 Contingency – £20,000 |

Common Risks with CSA

For Contractors:

- Front-loading: Overloading profit into early works (e.g., foundations) can disrupt cash flow expectations.

- Missing scope: Items clearly in the Employer’s Requirements but left out of the CSA won’t be reimbursed.

- Valuation disputes: Lack of breakdown can lead to under-certification if QS challenges your application.

For Developers:

- Overpayment risk: If the CSA is front-loaded, you may overpay early for uncompleted work.

- Inaccurate variation pricing: Without cost detail, variations are harder to justify.

- Design development claims: Ambiguity can lead to disagreements about what’s genuinely new scope.

Real-World CSA Scenario

Scenario: A contractor submits a vague CSA with “External Walls – £200,000.” During payment appraisal, they claim 40% complete due to finished brickwork. However, the QS values it at only 20% because cladding and rendering aren’t started.

Impact: Disagreement leads to underpayment. Contractor’s cash flow suffers, and trust erodes.

Lesson: Break it down clearly. Use realistic allocations per element.

One-Page CSA Checklist (for Field and Office Use)

Pre-Tender:

- Use the Employer’s CSA template

- Itemise all key elements—avoid vague entries

- Cross-check with the latest design package

- Verify provisional sums and contingencies

Interim Payments:

- Refer to CSA line items in applications

- Substantiate % completed with actual progress

- Track Effective Contract Sum after variations

Watch Out For:

- “Included above” or blank CSA lines

- Overloaded early-stage values (front-loading)

- Items priced too low for realistic buildability

Best Practices:

- Submit with detailed backup if CSA is high-level

- Raise queries on suspect line items during review

- Keep CSA aligned with updated design documents

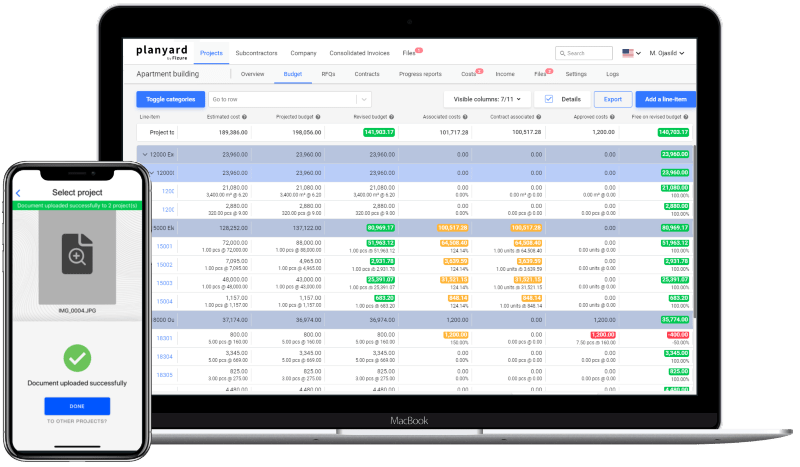

How Planyard Helps with Contract Sum Analysis

A clear, structured Contract Sum Analysis isn’t just a contractual formality—it’s your frontline defense against valuation disputes, cash flow surprises, and margin erosion.

With Planyard, you can move beyond error-prone spreadsheets and manage your CSA with confidence. Our platform lets you upload your project budget in your preferred structure, automate cost tracking, and monitor real-time variances across subcontracts, purchase orders, and valuations.

To support different workflows, Planyard allows users to define both High-Level CSA Entries—ideal for early-stage tendering—and Detailed CSA Entries that link directly to subcontractor packages and help with day-to-day cost management. This flexibility means your CSA can evolve alongside your project, from tender through to completion.

Whether you’re submitting interim applications or assessing variations, Planyard ensures your CSA stays aligned with the actual progress and design evolution—saving you time, reducing disputes, and protecting your bottom line.

Ready to take control of your CSAs and project financials?

Start your free 14-day trial of Planyard today—no credit card required. Or, book a demo to see how easy it is to streamline valuations, track variations, and stay on top of your margins.